In any large change to an industry, the issues that keep cinema owners awake at night are not those directly in front of us, as we can plan and mitigate those risks. It's the unexpected consequences that you don't see coming that wake cinema owners at 3am with their mind racing. "Have I missed something?"

In this article I will articulate an unexpected consequence of the pandemic and subsequent rise of the streamers. I will then make some general observations on how this is likely to affect theatrical exhibition. Obviously it's not good, but it is nowhere near as bad as it looks.

The theatrical cinema comeback

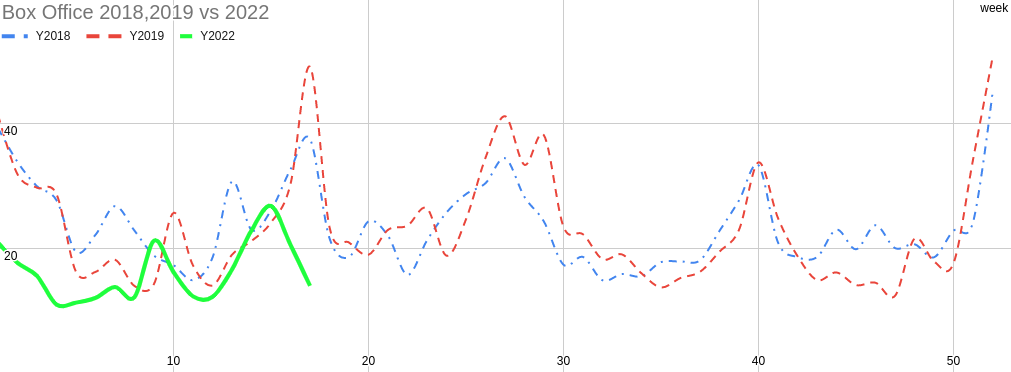

There is no doubt that cinema is powering back. In Australia, the COVID crisis is now behind us and has been for about 4 months. Australia is currently tracking at 30% down on 2019 levels but is expected to pull back to near 20% due to the extremely strong slate coming over the northern hemisphere summer.

A recently AMC analysis released similar results (See recent AMC industry analysis here). Like Australia, they are currently tracking lower at 40% down on pre-pandemic levels but expects this to improve. The author, based on AMC's performance and comments, expects the "new-normal" for cinema attendance will permanently be 20% below pre-pandemic levels.

This drop in attendance/gross was covered in industry predictive analysis I posted back in 2021 and is recommended reading if you would like a more detailed understanding.

- Cinemas After Breaking Windows - Read HERE

- By the numbers, what we can expect for cinema attendance after vaccinations - Read HERE

Cinema is alive and well, however, there are significant changes in average visits per year per person. This is very manageable and the industry will adapt. CinemaCon recently happened and many trends were identified in terms of how the current industry is adapting to these changes.

Some significant trends that were discussed at CinemaCon 2022:

- John Fithian of NATO again restated with absolute conviction that date-of-release streaming was dead and piracy killed it. (Streaming anywhere, Piracy everywhere) (Read More)

- In an industry panel it was indicated many larger cinemas are closing screens to convert a portion of the complex into food/restaurant facilities.

- The industry is struggling with the change in culture as restaurant quality staff are older, harder to find, more expensive and in general result in less profit than historical cinema operations.

These trends make it clear that cinemas are evolving into entertainment complexes and are offering more than cinema only. This trend was also apparent before the pandemic as new builds tended to focus on the entertainment complex. With the current environment, this trend is expected to accelerate.

Industry expectations

Content is king. With the forced closures of cinema over the last few years, exhibitors expect a treasure trove of great content on our reopening. Cinema was closed but the production industry was still going if only at a reduced pace. Considering we have nearly 2 years of production backlogged, it was expected the better of the films over the two years would all land in 2022. All things being equal, if conditions were like pre-pandemic levels and with so much high quality content, 2022 had the potential of being the best on record.

Unfortunately the current trends in attendance do not indicate this. However we still have 2/3 of the year to go and a very strong slate coming during the northern hemisphere summer.

Personally as a cinema owner, I was hoping we could approach pre-pandemic levels, even despite the fall-out of the pandemic. This may still be possible but with the collapse in content being released this year, it's not looking as likely.

The Content Collapse

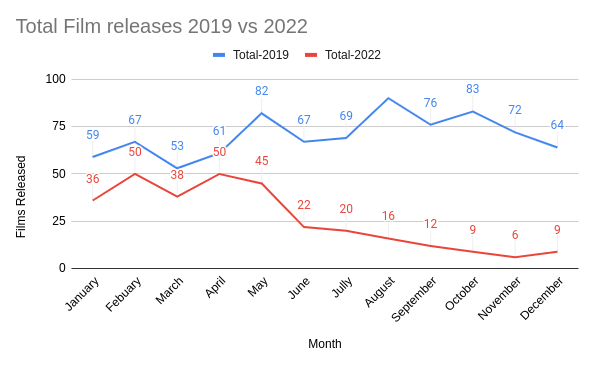

Following is a graph based on the Australian market, but expected to be similar around the world, of the number of films being released each month comparing pre-pandemic 2019 as a reference and 2022, being the post-pandemic environment. It must be noted that Australia has one of the highest vaccination rates in the world plus one of the lowest infection rates. In other words, Australia should be ahead in most metrics in consideration of going back to pre-pandemic levels.

WARNING: This data is based on current registered releases of films to the theatrical market as of April 28, 2022. It is possible it could significantly improve, however historically this is unlikely (Read below). However, as this is the first year after the pandemic, there could be more films dropped. (Here's hoping)

NOTE: CinemaCon has just finished. This data was taken specifically after CinemaCon announcements and likely changes to the release slate occurring.

From January to May, theatrical film releases have only managed about 75% of pre-pandemic level. This would fall into line with current Australian gross performance also being approximately 30% down on pre-pandemic levels. (See live gross performance graph here)

From May 2021 onward, the number of films being released to the theatrical market has declined significantly.

For readers unfamiliar with the release slate, typically films are placed on the slate 6 months to many years before the release date so distributors can plan when to release their film in relation to other larger films. Also, a film typically needs 6-9 months of planning and marketing. Major films typically need a solid 12 months or more. Indy films can be 6-9 months. Either way, from the date of the data capture, the slate is unlikely to change for at least 9 months into the future for Indy and 12 months for Major distributors. In other words, the slate up until Christmas, historically by this time of the year, is cooked in and unlikely to change much.

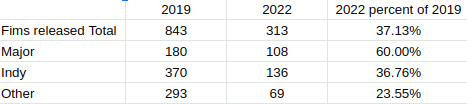

With the 2022 release of films slated to be 37.13% of 2019 levels, content being the fuel that runs the theatrical industry, obviously cinema exhibitors are not going to turn over as much money either.

To get a clearer picture on this, let's split this into major studios and indy distributors to give us a clearer picture of which markets have been affected the most.

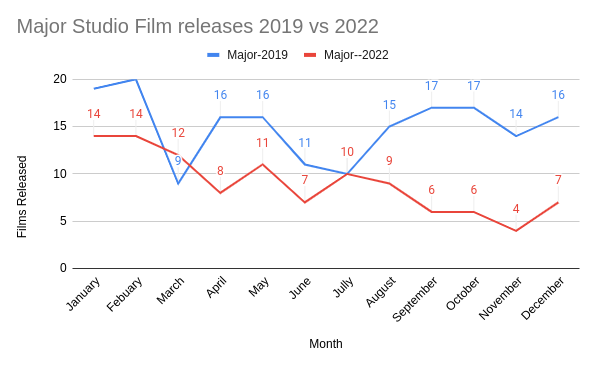

The Major Distributors

NOTE: December is extremely low, however, this is attributed to the release date of Avatar 2, which is expected to grab the bulk of the attendance, and as such, other studios are likely staying clear leading to an unusually low month.

The major studios appear to have a solid release schedule with constant films coming out though the year. However, it is far weaker than pre-pandemic levels. The end of the year also shows an unusual reduction in films for release. With the pandemic still fresh in our minds, it is hoped that some more films will be dropped into the weaker 4th quarter of the year. But typically cinema owners would expect everything to be set in stone for that period by now.

This lack of releases can be partly attributed to the change in policy by many major studios who now have streaming companies they also need to feed. Numerous titles that once were slated for theatrical are now streaming exclusives. For example, some Pixar content and numerous Star Wars releases that were once expected to be films are now destined for Disney Plus, typically drawn out into an 8-10 episode series.

Considering the large number of higher quality films on offer this year, we could also attribute the lower number of releases in the major market as a side effect of the strong belief in the current slate. Due to this they are giving these films a wide berth as they do not want to cannibalise one popular film with another. This is resulting in less perceived room for content. As an example, November is extremely low in major releases as Avatar: The Way of Water is being released in that month and is expected to pull all the air out of the market.

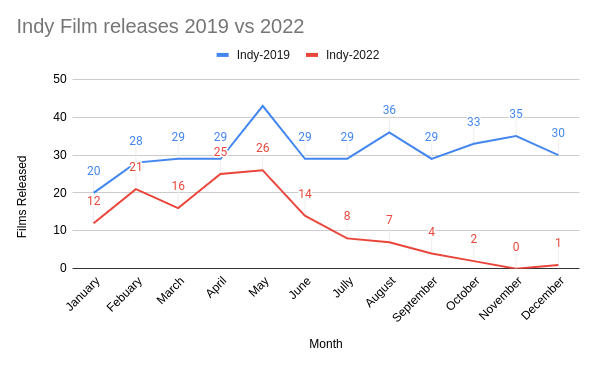

The Independent Distributors

The indy film market appears to be where most of the contraction is occurring. From June onwards there is a steep fall of in mid tier films. i.e. art house, family, comedy. As a cinema owner this is especially worrying as this variety of films, although not big money makers, would bring in a regular cinema goer more frequently. This supplies the industry with a consistent income over the peaks obtained from the major blockbuster films.

Without a constant variety of films, cinemas become far more reliant on the major blockbuster films. Films that all too often flop. The risk in running a cinema, especially smaller cinemas, is that if you land a few blockbuster flops in a row, you're under water. Pre-pandemic, the constant variety and regular attendance for the mid-tier was enough to keep the doors open when this occurred. Due to fewer mid-tier films filling the gaps between blockbusters, running a cinema has become a lot more risky. And with risk comes price rises to mitigate those risks. Commercial viability will also need to be re-evaluated.

Due to this unprecedented drop of in mid-tier films, I reached out to numerous independent distributors to comment on this trend. From their perspective, there is always a constant stream of indy films, and even if the slate is unusually low compared to historical behavior currently, with film festivals occurring and the large number of indy films that get released every year, they expect reasonable up-tick in coming months.

This is good news, however, it does not address the metrics below. The cause for the suppressed mid-tier content is likely still in play.

More metrics

The conclusions above are not all based on the data I have collected. Time to pull in other data from the industry to help clear up the meaning of what these graphs are likely to indicate.

OMDIA

In a recent "Cinema Technology" online trade magazine (Click here to open), David Hancock of OMDIA, a cinema industry analytics company, stated the following metrics.

Quote:

"The top 10 films take around 30-35% of the box office in a normal year and this rose to 53.1% in 2020 and 46.7% in 2021. This metric was rising due to the dominance of the leading films within the premium space (i.e. higher ticket prices) but if this continues for the long-term, this percentage remaining around half of the market would be a concern." - David Hancock

In effect this indicates that many mid-tier films likely lost money on their theatrical release. It is no surprise these films are now looking for alternate paths to profitability, ie. going straight to streaming services instead of having a theatrical release.

Sundance and other film markets

Considering the poor performance of mid-tier films and the cashed up streamers, 2021 was a big year for streaming companies buying up a significant portion of the films that hoped for a theatrical release. For example, AppleTV's purchase of the academy award winning film, CODA.

Los Angeles Times - "Can studios compete with streaming services to buy this year’s Sundance hits?"

Quote:

"Traditional studios that lean heavily on the theatrical business could find it even more difficult to bid against deep-pocketed streaming services this year"

Is this a permanent trend?

Probably not, but only time will tell. The recent news regarding Netflix's share price tumble, plus other media companies having considerable declines, is likely to significantly reduce the amount of money the streamers are willing to pay for mid-tier films. This is great news, however, I do not expect them to stop trying. If mid-tier films continue to do poorly in the theatrical environment, we can still expect a considerable defection to the streamers with their guaranteed return.

The current 20-30% reduction in gross appears to be reasonably stable and long term. Many cinemas, not all, are likely able to cope with this reduction in attendance, hoping that attendance will increase in the coming years. However, as David Hancock (OMDIA) indicates, if the lack of content also becomes a permanent fixture of the industry, it will be very concerning indeed.

Outlook

If the current trends in the market hold, we are looking at considerable pain and a likely change in the cinema industry. If we consider the trend above does hold, and the cinema industry does lose a significant number of films to streaming moving forward, what can we expect to happen with the cinema industry?

Large multiplexes with many screens will suffer

With less content, comes the need for fewer screens. A lean car engine has fewer cylinders. With fewer films to show, many multiplexes with 8 or above screens may find they have more screens than is needed to service the content on offer to the population they service. Those extra unused screens are now a noose around their neck as they still need to make enough money to service the costs of the extra real-estate and external costs they generate. This is likely to result in multiplexes closing or downsizing, giving large sections back to the complex for re-development or redevelopment of the site themselves into a multi-service business or entertainment complex.

Premium Large Format (PLF) becomes more important.

With the shift towards blockbuster films being a larger part of the profit engine of a cinema, the PLF segment is likely to become a major growth area to win over the consumers and the fewer visits per year to the cinema they attend. For many, attracting this limited resource will become a sink or swim endeavour.

Cinema becomes the side, and not the main course

As the industry shifts to reliance on blockbuster films, a cinema that is only a cinema becomes less sustainable. An example of this is already apparent as most of the new cinemas opening in the world are not just cinemas, they are entertainment complexes. They offer numerous experiences such as restaurants, gambling, bowling etc. Cinema is now one of the many attractions on the menu.

This is likely the future as, if cinemas are now entering a boom or bust type existence, the business needs other alternate income streams to hold them over when the content is not working. If the cinema is only 1/3 of the business and it is doing poorly, only 1/3 of the business suffers and no cash flow issues exist. On the other hand, if you are only a cinema, you are in deep trouble.

This trend has deep and long term ramifications for the incumbents as their multiplexes are cinema-only type infrastructure. To build a multi-entertainment complex, it is basically start from scratch and build a different building. It will be a hard pill to swallow for the incumbents to write off the crystal palaces we call multiplexes today. Many locations are already attempting to pivot to this future, but many are simply not in a position to do so. Expect buyouts and amalgamations as less suitable locations are abandoned or completely redeveloped.

Small cinemas in a better position

Small cinemas are like a smaller car that is far more fuel economical, needing less to go the distance. With less content, they are in a better position to maintain a similar gross turnover. Typically they were not in a position to play all the films anyway. This is good news as even with the lack of films, many regional cinemas should be able to more easily deal with this change. However, other factors will also need to improve. The 45-day windows, and common 3 week restrictive access and onerous policy requirements will need to be reduced to match the lower visit per year per person level that is the new normal for the industry. To overcome this, smaller cinema will be required to play more films over a shorter period. This will allow them to be more appealing to more potential customers allowing them to maintain a similar attendance level.

Conclusion

CinemaCon was very reassuring. The trends and issues discussed did indicate that although the industry is going through some changes, the industry is raising to the occasion and adapting to these changes.

As a cinema owner myself, I hope in sharing this analysis so that other cinema operators who may not have the capability to discover these trends in the data can use these insights to make better informed decision on how they will deal with our evolving industry.

James Gardiner

Small Cinema Owners (SCO)

3 comments

Showbiz Sandbox 585: Entertainment Industry Stumble Into Sociopolitical Pitfalls - Showbiz Sandbox : Showbiz SandboxJune 8, 2022 at 1:21 pm

[…] The Content Collapse – Unforeseen Consequences of the Streaming War on Theatrical Cinema https://www.smallcinemaowners.com.au/2022/05/06/the-content-collapse-unforeseen-consequences-of-the-… […]

DCP Digital Delivery is top topic at Australian International Movie Convention (AIMC) – Small Cinema OwnersJune 28, 2022 at 3:31 pm

[…] theatrical market. (See a recent SCO article looking at the hard numbers in regard to these trends: The content collapse – unforeseen consequences of the streaming war on theatrical c… – […]

DCP Digital Delivery is Top Topic at Australian International Movie Convention (AIMC) - Celluloid JunkieJune 28, 2022 at 6:16 pm

[…] theatrical market. (See a recent SCO article looking at the hard numbers in regard to these trends: The content collapse – unforeseen consequences of the streaming war on theatrical c… – […]