It's a difficult time for cinema owners. From large cinemas to small, there has been very little good news. SCO newsletters have been sparse, as we all know it's bad. Why tell you what you already know? Even so, in the same way we need health experts' input into how the COVID crisis is going to affect us, it's time to visit some of the performance stats in the Australian market to help us understand what our exhibition business faces going forward.

Obviously there are challenges ahead, and the following numbers and graphs will indicate as such, but there is some good news, specifically for smaller cinemas, that will be covered in the following analysis.

Finally, SCO has not been idle. Identifying the difficulties ahead, SCO has been putting time into a free-to-use tool specifically targeting smaller cinemas. It is my hope that this will save you time and make your cinema more productive, despite any loss in patronage, resulting in a sustainable cinema industry and culture going forward.

Australia, an indication of what is to come for the rest of the world

Australia has been a very lucky place in terms of COVID. Our island status has made it possible to build “Fortress Australia'': we have managed to all but eradicate COVID, apart from the occasional outbreaks from overseas quarantine that are typically brought under control within weeks. Australia has largely been open and trading, with activity in some regions almost back to normal.

However, for Cinema, it's nothing like before COVID. And here is where we need to look at one of the first key metrics.

Currently the news is full of positive sentiment as cinemas are opening in other parts of the world, typically to areas where COVID is still in circulation but at a controlled level. Initial patronage in these opening markets is good, and there appears to be a high level of consumer excitement to get back out into the world, including cinema. There is an expectation cinema attendance will simply bounce back to, or near to, pre COVID levels.

Australia historical numbers are a good indication of exactly how this will likely result. We are open, and have been open for a long time. Did we see a hump? Did attendance return to previous levels? Should the rest of the world expect the same behaviour?

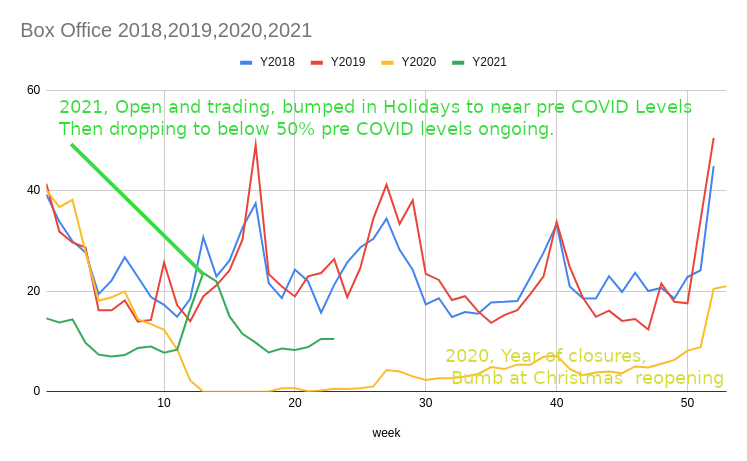

The following graph is the performance per week GROSS for cinemas in Australia.

We are nowhere near the previous levels. Based on Australian performance graph, let's look at these questions again.

- Have we seen a bump as we open? - Yes but not substantially.

- Have people returned to pre COVID attendance levels? - No.

- Should the rest of the world expect the same behaviour? - Yes, likely.

This could largely be attributed to lack of quality content, i.e. tentpole films. However, we have been getting some decent tentpole content which, depending on the distribution model, has been giving us some mixed results.

As an industry trying to get back into profit, these numbers are poor with a perceived performance of less than 50% of historical levels. The key issue going forward, based on this graph, is that just opening up is not enough to sustain the industry. A lot of premium content has been delayed from release until more cinemas around the world are open. We need tentpole content to be turned fully on before we can expect a substantial increase in patrons.

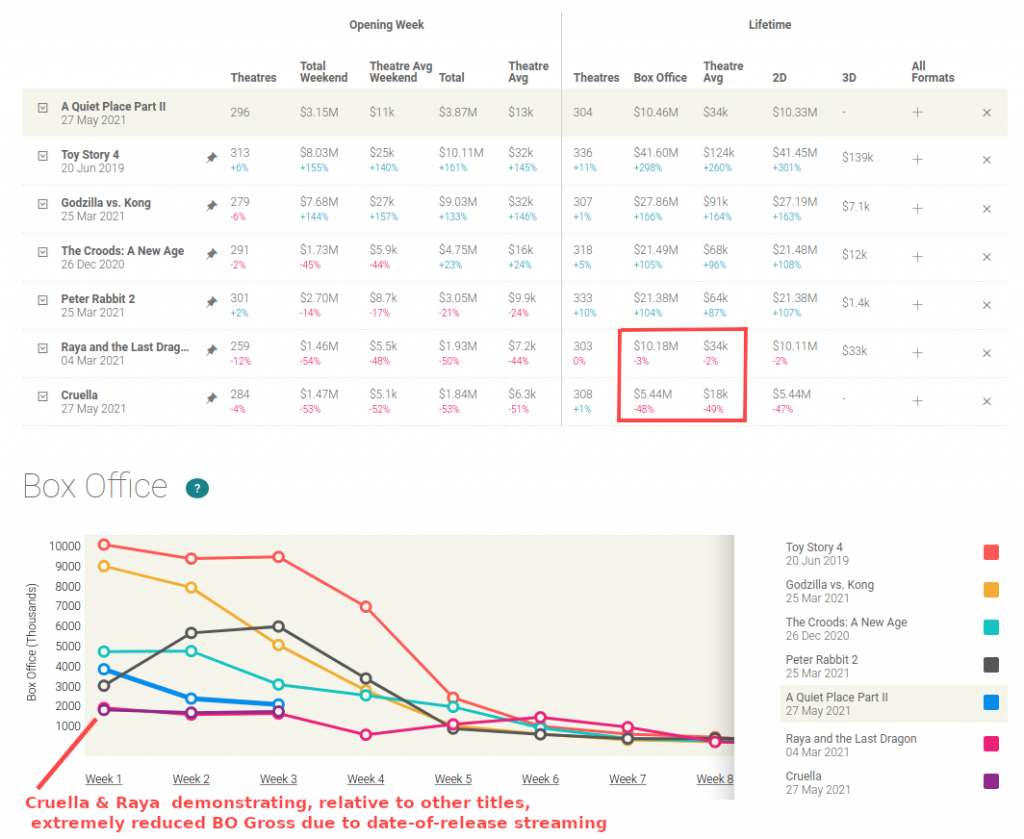

There is one other key metric to consider. The following graph is an indication of performance of a selection of films over the COVID period. Plus a reference film (Toy Story 4) to help put them in context.

Based on the graph above we can make a number of generalisations.

- Considering the films released during COVID are into a market with little to no competition from other tentpole films, you would expect a benefit to their gross due to the lack of competition. However, despite this lack of competition, the performance of Godzilla vs KingKong and Peter Rabbit 2 was not exceptional. They may well have achieved a much higher gross if released to a pre COVID environment.

- Looking at the impact of date-of-release streaming, Disney has Raya and Cruella as examples of this release model and how it affects the gross in exhibition. Focusing on Raya, it was arguably as good or better than other animated films released during the COVID period as indicated by how well it held during its release. However, Raya made less than half the gross of similar films in the same market at a similar time that had an exclusive theatrical window before being released on streaming platforms. This indicates that given the option of cinema or home, (whether that is Disney+ or piracy), the market did exactly what you would expect if given two options: half the potential audience chose to stream it at home, and half chose to see it at the cinema, resulting in an estimated loss of 50%+ of the expected gross for exhibition.

- As Cruella is a recent release, the numbers are only just appearing, however, it appears to have suffered a similar fate to Raya if not worse. It must be noted that Cruella is holding well. A sign that it is a good film that would have done exceptionally well in a pre-COVID market. Despite a strong cast and story, it has only managed to achieve under 50% gross compared to “A Quiet Place II”. Again, as an exhibitor in pre-COVID times, I would have expected Cruella to be 150-200% of “A Quiet Place II” Gross, not 50%.

- Date-Of-Release piracy, requires its own section below. As films appear to be underperforming to expectations before COVID, it is expected that piracy is part of the story that explains this. However, it is very difficult to estimate exactly how big a problem this has become due to the lack of availability of data from streaming platforms.

Streaming anywhere, piracy everywhere...

Can it last?

Piracy had significantly diminished before COVID hit. Legal paths to accessing content had replaced the piracy options as it was just as convenient to utilise. The 90 day window with the exceptionally strong, but expensive, security used in the digital projection of films proved to be effective in protecting the exhibition industry from pristine pirate copies appearing on the internet.

Piracy is very much a supply and demand problem. Before COVID, you had to watch it at the cinema, or wait until it landed on a domestic accessible platform, such as streaming. Now with date-of-release streaming, pirates can rip/copy the PVOD stream and typically make it available within 24 hours of its release to the world.

COVID lockdowns caused a 50% jump in piracy activity in many markets. With the availability of pristine pirate copies on the date-of-release of films, it is understandable that piracy activity has reacted to the increase in supply. See (https://www.hollywoodreporter.com/business/digital/online-piracy-spikes-coronavirus-lockdown-study-finds-1291961/)

Due to the lack of release of tentpole films, privacy activity has again diminished. This is expected to reverse as tentpole films, specifically those with date-of-release streaming, start to become available.

The impact of date-of-release piracy? This is completely unknown. Only the distributors with data on streaming numbers have enough information to make a reasonable guess. Otherwise, I would guess between 2% and 25%; there is no real way to know, especially in this environment with so many moving parts.

Can it last?

The estimated $20billion worldwide spent on implementing the DCI digital cinema solution and its military grade security is money wasted in a date-of-release streaming world. It is not surprising that studios are lining up behind the 45 day window. It is my expectation that date-of-release streaming will not be a common occurrence after COVID, however I do feel the studios will still utilise this path when it comes to bolstering their streaming platform dominance.

In my opinion, to a major studio board member, this behaviour may seem a reasonable sacrifice in film gross at the expense of keeping the sharemarket happy, share price high and streaming subscriptions up. As a cinema owner, I am extremely uncomfortable with this behaviour, but understand it is a characteristic of the changing times.

Looking at history, the formula will change.

Many readers have been cinema owners for a long time. Cinema will never die, but the business model of exhibition or running cinemas has changed numerous times over the years. TV, Colour TV, VHS, DVD…each time these new technologies surface, the attendance levels fluctuate to a new level of “reduced” demand as the market or menu of entertainment options available to consumers increases and cinema becomes more marginalised. Typically, this results in over serviced markets, and some exhibitors forced to close locations that are no longer commercial.

For example, when opening up a cinema in a region, the base formula to calculate the number of screens you should have is based on the number of people in the catchment area. In general, 10,000 people per screen is a good rule of thumb. This formula may change to 13,000 due to the lowering average attendance level per population.

This is already very relevant as some cinemas in the United States have made headlines as they enter chapter 11 (ie. go into administration), allowing them to close underperforming locations. After coming out of chapter 11, the cinema chains then typically announce opening new locations in under-serviced markets. See Alamo Drafthouse as an example.

It would be prudent for cinema owners to address this potential loss of revenue before it becomes a bigger problem.

How much will the attendance drop?

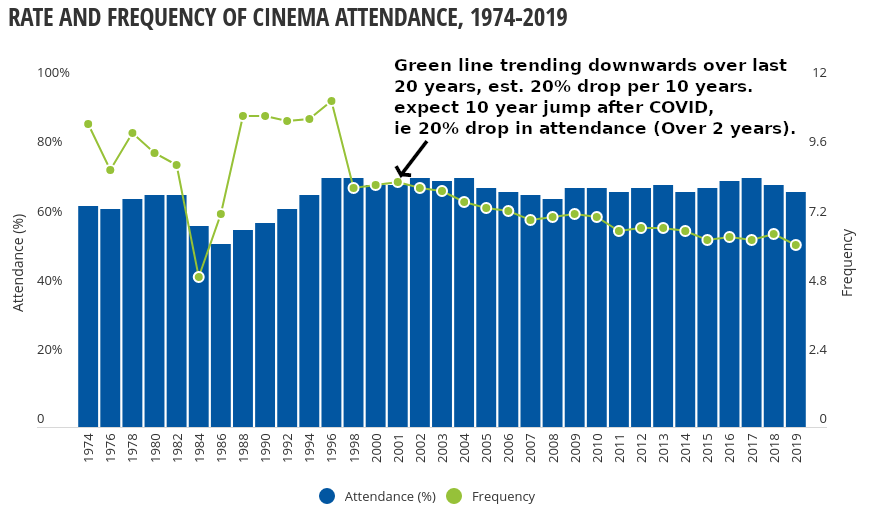

At this stage , the answer to this is still largely a guess. But let's give it a go. Based on Screen Australia's website we have a very telling page. “Audience Attendance Patterns”.

If we take the general trend, from an average of 7.4 visits per year in 2009 to 6.3 in 2019, this equals a drop of 1.1 visits per year over a 10 year period. I predict that COVID will greatly accelerate his trend, resulting in the same drop in average visits over 2-3 years, rather than 10. In other words, I would predict a drop of 1.1 visits per year between 2019 and early 2022, ie. 5.2, which is 20% lower than the average visits in 2019 (6.3).

Personally, I feel that's a safe estimation and as a cinema, you should be budgeting for such a trend AFTER the backlog of tentpole films pass.

45 day windows: an unknown quantity.

This is still the wild card in terms of what the future holds. Based on the effect of date-of-release streaming that splits the market 50/50, a greatly reduced window is not going to have the same effect but it will have some effect. 2%-25% reduction? It is difficult to say. Will it simply be absorbed into the 20% downward trend or be an additional drop? Again, there is no way to know. Only time will tell.

You said there was some good news.

As smaller cinemas and to an extent arthouse cinemas, we are far more likely to metabolize the transition in the industry. Smaller cinemas typically attract more discerning customers; for example, an older demographic or film lovers who go to the cinema for the theatrical experience. Larger multiplex locations are more reliant on customers who simply want to be entertained, for example, by seeing a particular film. These patrons are typically less concerned about the content and more likely to consider other experiences, (for example, streaming, ten pin bowling, mini golf, online gaming), thus leaving mulitplexes more susceptible to losing customers to other entertainment offerings. The estimated 20% drop is likely to impact multiplex locations more than smaller cinemas.

SCO’s free-to-use tools to help smaller cinemas.

SCO was started to help identify and give advice to smaller cinema of changes in the industry before COVID appeared. The trend in attendance has been going down for 20 years yet there has been little response to this decline. At some stage we need to react to this: COVID makes that time now. As an industry we need to adopt innovative and more productive processes to adapt to the changing world. That's what every other industry has been doing.

Tools developed by digitAll Pty Ltd and utilised by DCN to operate its regional cinemas are now available to SCO members. These tools implement a number of features usually found in large theatre management systems (TMS). I want to make these available to small cinemas worldwide at no cost and with no obligation. It is hoped that using these tools will save cinema owners 2-4 hours of work per week in labour.

The system requires a server running LINUX to run the tools on, and the cinema owners will need to install and set up the software themselves or with help from a technically competent individual. The system is well documented and should be easy to implement. I hope you find this useful, and welcome any feedback you have.

Please follow this link to find out more.

Cinema-catcher-app

News on Digital Delivery

Finally I would like to point out some major news on a big topic at SCO. In many newsletters over the years we have covered content delivery being a area of improved productivity and cost savings for running cinemas. Especially smaller cinemas. Recently there has been some major news in that the top companies in offering these services have all joined forces.

So what does this mean is yet to be known.

If you would like an analysis piece on this topic gat back to me.

Goodluck.

Finally, here at SCO we wish you the best of luck in the challenging times ahead.

Regards,

James Gardiner

www.smallcinemaowners.com.au

Email: james.gardiner@smallcinemaowners.com.au