After years of decline (2024 & 2025), uncertainty, and “wait and see” trading, Australian Box Office results show a clear lift in attendance through the first part of 2026. Not a one-off spike tied to a single title, but a broad-based improvement that is starting to change operator sentiment.

In today’s Small Cinema Owners (SCO) newsletter, I will examine this unexpected improvement, and over the coming weeks follow up with several additional articles on the structural changes currently reshaping the industry.

Eighteen weeks into the year, national attendance is running 12.5% ahead of 2025, even while still 24.6% below 2019 levels. Unfortunately regional cinemas, and specifically smaller cinemas, are seeing less of an increase. Growth is present, but not as strong as metro locations, suggesting that cost-of-living pressure, fuel prices, and reduced travel are influencing behaviour.

And yet, despite those pressures, regional audiences are still turning up.

That matters.

Because it suggests cinema is not simply benefiting from favourable conditions, it is improving even while meaningful economic headwinds remain. That does not mean those pressures are not real, but it does show the underlying demand for cinema has not disappeared.

The numbers: not a full recovery, but a real shift

| Year | Attendance improvement from prior year | Attendance vs pre-pandemic level |

|---|---|---|

| 2023 | 6.90% | -29.66% |

| 2024 | -2.09% | -31.13% |

| 2025 | -1.29% | -32.01% |

| 2026, 18 weeks in | 12.55%% | -24.64% |

This is not a return to pre-pandemic levels. But it is the first convincing directional shift upward in several years.

A 12% increase in a single year is significant, particularly for smaller cinemas that have effectively been operating in survival mode. For many, this level of uplift is the difference between standing still and being able to plan again.

With almost a third of the year now complete, the remaining release slate still appears stronger than average, suggesting the current 12% uplift may yet improve further by year’s end.

Deeper dive into the data

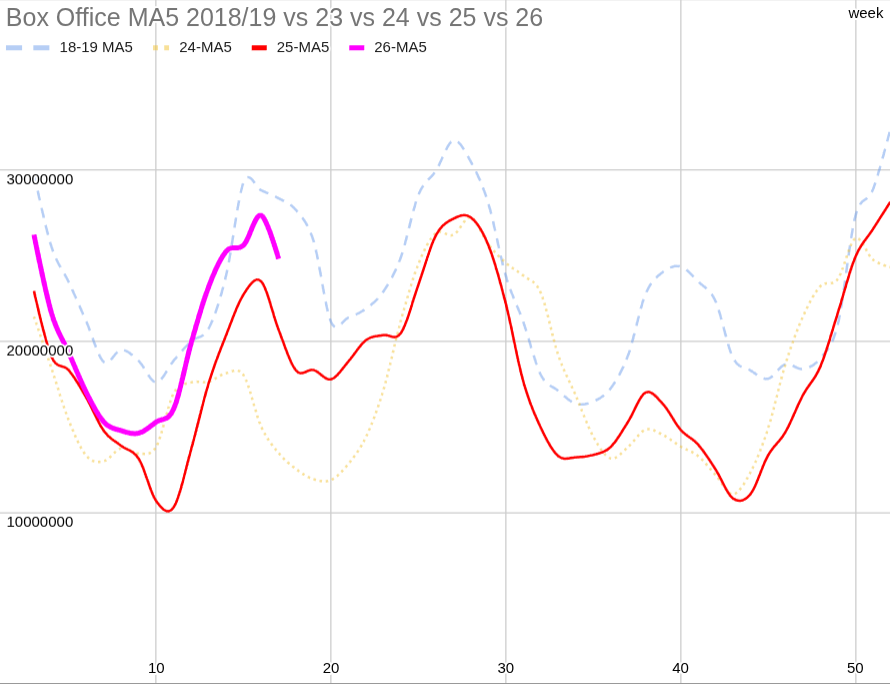

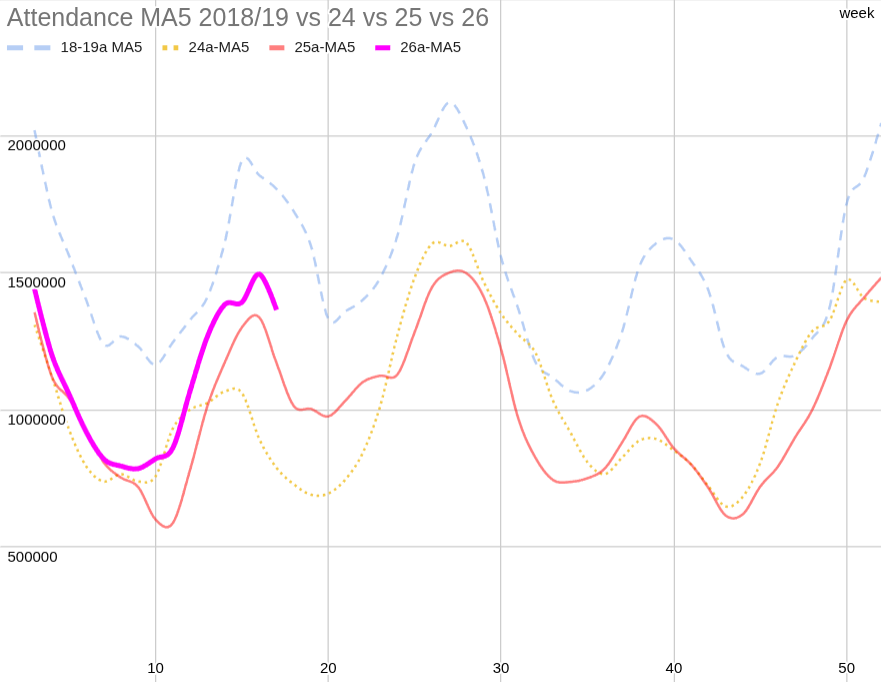

For those who enjoy numbers and graphs (like me), let’s take a closer look at the underlying data.

The following graphs compare:

- Weekly box office performance

- Weekly attendance trends

The divergence between attendance recovery and box office recovery is particularly interesting, and is something we will examine in greater detail in a future SCO newsletter.

| Attendance 2026 diff prev year | Attendance 2026 % diff prev year | Attendance 2026 diff from 2019 | Attendance 2026 % diff 2019 |

| 28994 | 1.56% | -883,508.00 | -31.90% |

| 144131 | 4.23% | -1,362,167.00 | -27.71% |

| 260127 | 5.45% | -1,913,409.00 | -27.55% |

| 409629 | 6.88% | -2,492,418.00 | -28.14% |

| 424725 | 6.26% | -2,746,079.00 | -27.59% |

| 426575 | 5.72% | -3,138,467.00 | -28.46% |

| 223705 | 2.60% | -3,355,654.00 | -27.52% |

| 213805 | 2.27% | -3,528,109.00 | -26.83% |

| 473478 | 4.74% | -3,640,771.00 | -25.80% |

| 635881 | 6.03% | -4,475,932.00 | -28.59% |

| 763247 | 6.90% | -4,947,292.00 | -29.51% |

| 1331583 | 11.47% | -4,761,877.00 | -26.89% |

| 1584589 | 12.84% | -5,026,065.00 | -26.52% |

| 1912939 | 13.76% | -4,584,022.00 | -22.47% |

| 1906489 | 12.21% | -4,615,676.00 | -20.86% |

| 1823652 | 10.78% | -5,376,673.00 | -22.30% |

| 1789408 | 9.88% | -7,099,314.00 | -26.29% |

| 2388956 | 12.55% | -7,003,623.00 | -24.64% |

Below are graphs showing attendance trends for pre-pandemic and the more recent years. There are 2 graphs, 1-BoxOffice take, 2-Attendance. These are very interesting as the difference in attendance compared to Box Office turnover numbers needs more scrutiny. We will dig into this in a future newsletter.

Streaming is no longer a land grab, it’s a profit business

One of the biggest structural changes underpinning this recovery is happening outside cinemas.

Streaming has changed.

For years, the model was simple: acquire subscribers at any cost. Volume mattered more than profitability. Content spend expanded rapidly, and films that would traditionally have gone theatrical were redirected to platforms as part of a global “land grab.”

That phase has now weakened in the current economic environment. The focus has shifted to return on spend and profitability. This is not unexpected. In a more constrained economy, survival and margin matter more than scale.

It is no longer about capturing as many subscribers as possible, it is about building a business that can sustain itself through a downturn.

Streaming companies are under pressure to deliver profit, not just growth. The focus has shifted to ARPU (Average Revenue Per User), cost control, and margin expansion. The consequences are already visible:

- Price increases across major platforms

- Advertising tiers becoming standard

- Crackdowns on password sharing

- Reduced content spend and tighter greenlighting

Industry reporting through 2025–2026 shows that major platforms have cut content budgets, cancelled projects, and reduced overall output, with a clear pivot toward fewer, higher-impact titles rather than sheer volume.

And for the films that are being produced, there is a more disciplined approach to monetisation. Fewer are being sent direct-to-streaming, with greater emphasis on leveraging theatrical release and the visibility that comes with it.

There is also evidence that the start of 2026 has delivered fewer streaming titles that audiences find compelling. As platforms reduce output and tighten budgets, the volume of content may still appear high, but the perceived quality and cultural impact has become less consistent.

That matters. When consumers are unsure whether a title is worth their time, they become more selective. In that environment, cinema benefits from being seen as a more reliable, curated experience, where the content has already passed a higher commercial and creative threshold.

Fewer films, but more discipline, and that benefits cinema

During the streaming boom, a significant number of films that would have performed theatrically were instead pushed directly to platforms. In many cases, those films were used to drive subscriptions rather than maximise their individual return.

From a film economics perspective, that often resulted in films being under-monetised relative to their full potential.

Theatrical release has consistently shown that it does more than generate box office revenue. It builds awareness, creates cultural relevance, and significantly improves downstream performance across digital rental, streaming, and physical formats.

The industry now has enough data to support what was once debated:

Films that go theatrical first tend to perform better across their entire lifecycle.

Studios are responding.

We are seeing a rebalancing toward theatrical windows, not just for tentpoles, but increasingly for mid-tier titles that were previously diverted to streaming. The logic is simple:

- Theatrical creates marketing impact that streaming alone cannot replicate

- A cinema release acts as a quality filter for audiences

- Downstream value is higher when a film has had a theatrical presence

In short, theatrical is no longer seen as optional. It is being re-recognised as adding value across the entire lifecycle of a film.

Audience perception is shifting as well

At the same time, audience behaviour is changing in a more specific way.

It is not simply that consumers are becoming more critical of streaming. It is that confidence in new, up-front content on streaming platforms is becoming less reliable.

When a new title appears on a streaming platform, there is less confidence that it will be worth the time.

That matters.

Because when audiences are actively looking for something new and compelling to watch, they are increasingly turning to cinema as the more reliable option. A theatrical release carries a stronger signal, it has been more heavily selected, more heavily marketed, and has already demonstrated a level of confidence from distributors.

Cinema does not guarantee quality. But it reduces the risk of disappointment.

In an environment where consumers are prioritising time and value more carefully, that distinction becomes important. And it helps explain why attendance is improving even while broader conditions remain constrained.

Regional behaviour tells an important story

The regional data adds another layer to this recovery.

While metros are currently outperforming, regional locations are still seeing growth despite facing stronger economic headwinds. Higher petrol and diesel costs, combined with broader cost-of-living pressure, appear to be reducing long-distance travel and holidays.

But that spend is not disappearing entirely.

It is being redirected locally.

Cinema sits in a unique position here. It is:

- A relatively low-cost outing compared to major leisure spend

- A controlled and predictable experience

- Accessible without long-distance travel

This aligns with historical patterns. In economically constrained environments, cinema has often remained resilient because it offers affordable escapism.

That appears to be playing out again.

A lifeline for smaller cinemas

For independent and regional operators, this improvement is not just encouraging, it may be critical.

Many cinemas have spent the last few years in a holding pattern:

- Deferred maintenance

- Delayed projector upgrades

- Reduced staffing

- Minimal reinvestment

A sustained lift in attendance, even if still well below 2019, changes the equation.

It provides:

- Improved cashflow stability

- Greater confidence in forward bookings

- A pathway to reinvestment

If the current trend continues through the rest of 2026, it is likely that we will see more sites move out of “zombie mode” and begin planning for the future again.

The risk: energy and the broader economy

There is, however, a significant risk sitting over all of this.

Australia’s reliance on diesel is among the highest in the developed world on a per-person basis, reflecting the structure of the economy and its dependence on road freight, mining, and agriculture. That makes the country particularly exposed to fuel price shocks and supply disruptions.

If the current global tensions escalate into a more severe energy crisis, the downstream effects could be substantial:

- Increased operating costs across all sectors

- Higher food and essential goods prices

- Reduced discretionary spending

Cinema has historically been more resilient than many industries in downturns, but it is not immune.

The current recovery is happening despite these risks, not in their absence.

The real story of 2026

The key point is this:

Cinema is not back to pre-pandemic levels. But it is no longer drifting downward.

Attendance is rising. Streaming is being forced into a more disciplined, profit-driven model. Content volume is shrinking, but quality and theatrical prioritisation are improving. Audiences are reassessing value.

All of these factors are aligning in cinema’s favour.

For the first time in several years, there is a credible argument that the industry is not just stabilising, but beginning to rebuild.

Not a return to 2019.

But the first genuinely convincing recovery signal the industry has seen in years.

Before I go, I would also like to remind smaller cinemas of a few special offers SCO currently has available.

We have a limited number of refurbished Dolby/Doremi DCP2000 and GDC SX-2001A digital cinema player servers available in as-new condition for $500 each plus shipping.

We are also offering free CRU enclosures for cinemas needing replacements for failed or damaged units. These must be installed into a server. If interested, please contact me and I will have units prepared for dispatch. You simply need to arrange courier collection.

I also hope everyone has a productive and enjoyable Content Showcase presented by Cinema Association Australasia. I will be attending the Melbourne event on 12 May for a few days, so please feel free to come and say hello.

James Gardiner

Principal, Small Cinema Owners